Faculty & Research

Faculty & Research

As ESG retreats and heatwaves ravage Europe, companies are talking about extreme weather more than ever

By Shan Hongyu

Europe’s latest heat wave is not simply a weather story. It is a story of human loss and mounting economic cost.

The World Meteorological Organisation reports Europe’s late-June heat wave shattered temperature records and affected human health, agriculture, ecosystems, infrastructure, and labor productivity. Climate extremes are also becoming macroeconomic events: Reuters reported that heat waves, droughts, and floods reduced Europe’s economy by about 0.3 percentage points of output last year.

Ironically, these extremes are arriving just as ESG principles appear to be in retreat across both politics and business. Nevertheless, for companies, the costs of extreme weather events translate into issues around worker safety, lower productivity, higher electricity demand, transport delays, insurance claims, supply-chain disruption, and damage to physical assets. Extreme weather and natural disasters are therefore not only a climate or public health issue. They are becoming a financially material corporate risk.

A Growing Divide Between Transition and Physical Climate Risks

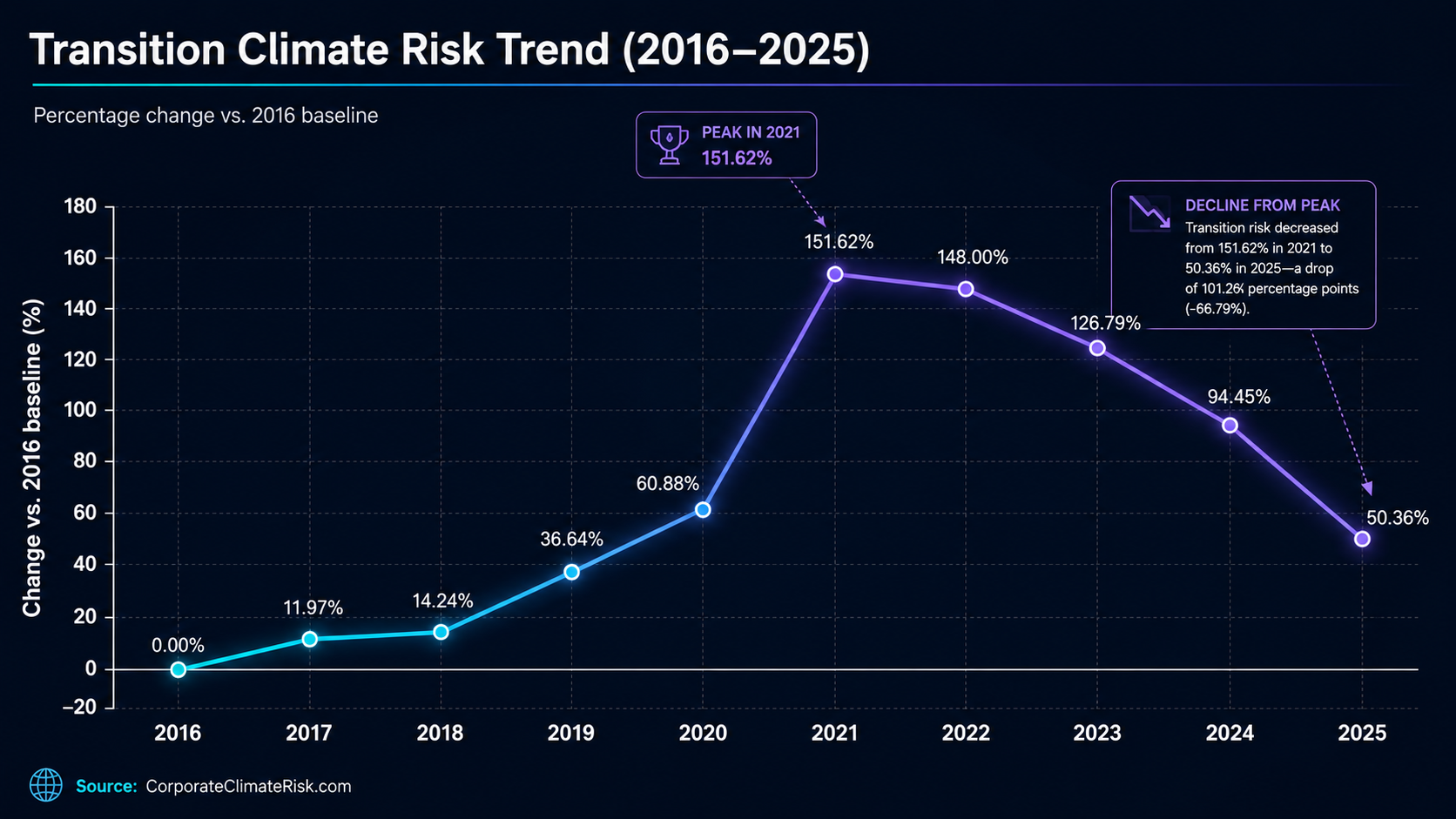

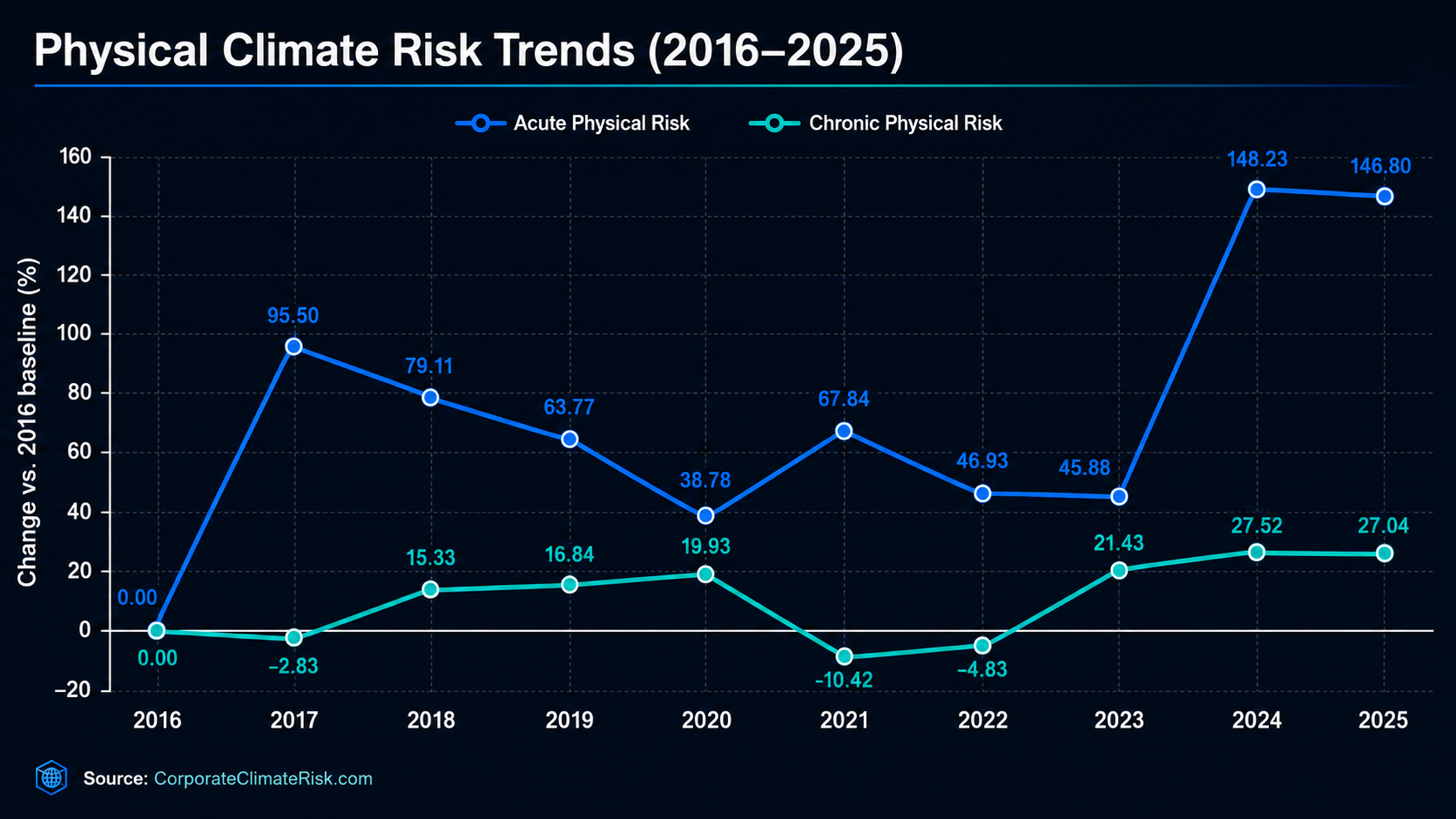

This shift is reflected in what companies themselves are discussing. Data from my website CorporateClimateRisk.com reveals a striking divergence between two types of climate risk: transition risk versus physical climate risk. Since 2023, corporate attention to transition risk — risks related to regulation, carbon policy, clean technology, and the move toward a low-carbon economy — has fallen substantially. At the same time, attention to physical climate risk rocketed near historical highs. Compared with 2016, corporate attention to acute physical risk was about 147% higher in 2025, while attention to chronic physical risk also stayed close to its record level. The data, covering all public firms on a quarterly basis, are updated through 2025Q4 and are made publicly available to researchers, investors, and policymakers.

This divergence reflects the fundamentally different nature of these risks. Transition risk is partly shaped by regulation, investor pressure, disclosure rules, and ESG politics. When the political momentum behind ESG weakens, companies may have less reason to discuss carbon policy, renewable energy targets, or decarbonization. Physical climate risks, however, are driven by the weather itself, such as heat waves, floods, wildfires, storms, and droughts. Governments can delay climate regulation; they cannot delay the next heat wave.

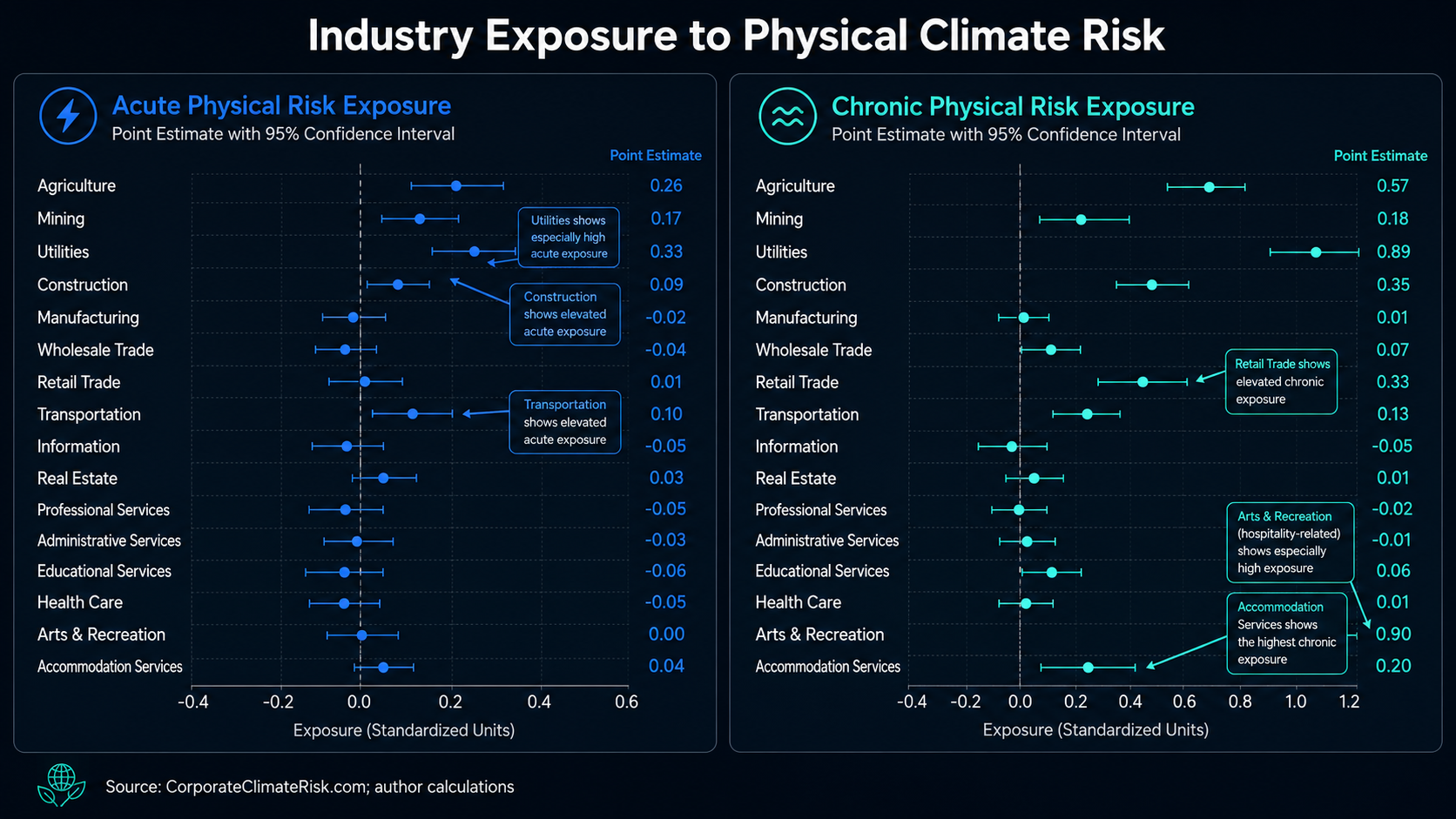

The data also reveal important differences across industries.

Acute physical risk tends to hit industries whose assets and operations are immediately exposed to sudden climate shocks. Utilities stand out prominently because power grids, transmission lines, substations, and generation assets are vulnerable to storms, wildfires, floods, and extreme temperatures. Construction and transportation are similarly exposed. Construction sites depend on outdoor labor, materials delivery, and weather-sensitive schedules, while transportation networks are disrupted by storms, flooding, damaged roads, port closures, and extreme heat affecting railways and logistics.

These are not abstract ESG concerns. They are operational risks that can stop production, delay projects, and raise costs.

Chronic physical risk presents a different industry map. It reflects persistent or recurring climate conditions rather than one-off shocks: warmer summers, abnormal winters, changing precipitation patterns, water stress, and long-term shifts in weather variability.

Retail and hospitality emerge as particularly exposed sectors. Retailers are affected by shifts in foot traffic, cooling demand, inventory needs, consumer behavior, and store-level operating costs. Hospitality is even more directly exposed: hotels, resorts, restaurants, and leisure businesses depend on comfort, travel patterns, water availability, and the attractiveness of destinations. Chronic heat can shorten tourist seasons, increase air-conditioning expenses, reduce outdoor activity, and force businesses to adapt their service models. In other words, acute risk breaks things suddenly; chronic risk changes the conditions under which entire business models operate.

In simple terms, acute risks disrupt operations overnight, while chronic risks gradually reshape entire business models.

These findings are consistent with my research paper with Qing Li, Yuehua Tang, and Vincent Yao, “Corporate Climate Risk: Measurements and Responses”, published in The Review of Financial Studies. Using earnings-call transcripts, we measure firms’ exposure to acute physical risk, chronic physical risk, transition risk, and firms’ proactiveness in responding to climate risk. Our research shows that firms facing greater climate risk are valued at a discount, especially when they fail to respond proactively. Proactive firms behave differently through investment, green innovation, and employment. The paper has become the second-most-cited paper among all articles published in the top three finance journals in 2024.

Climate Strategy Must Be Two-Dimensional

The implication is not that companies should abandon climate risk planning just because transition-risk discussion has declined. Rather, it is that climate strategy must become two-dimensional.

The first dimension is mitigation: reducing emissions, improving energy efficiency, investing in cleaner production, and preparing for future policy tightening. Second is adaptation: protecting workers from heat stress, redesigning facilities, hardening infrastructure, diversifying suppliers, improving water management, upgrading cooling systems, and building operational resilience against extreme weather.

While mitigation addresses the causes of climate change, adaptation addresses its consequences. Firms need both.

What Should Global Leaders Do Differently?

Global leaders should begin by separating climate risk from the narrower politics of ESG. ESG as a label may rise or fall with elections, investor sentiment, or regulatory cycles. But physical climate risk is not a branding exercise; it is a material risk to infrastructure, labor, supply chains, insurance markets, and corporate valuation. Policymakers should therefore treat climate risk less as a disclosure slogan and more as a core part of economic resilience. This means improving the quality of climate-risk data, requiring more comparable corporate disclosure, and encouraging firms to report not only emissions targets but also exposure to heat, floods, wildfires, droughts, and other physical shocks.

Furthermore, governments and business leaders should give adaptation the same strategic importance that mitigation has received. Reducing emissions remains essential, but many climate shocks are already affecting companies today. Public investment should therefore focus on heat-resilient cities, stronger power grids, flood defenses, water infrastructure, early-warning systems, and worker-protection standards. Firms, meanwhile, should conduct stress tests of their facilities, suppliers, logistics networks, and labor practices under more frequent and severe weather events. The goal is not merely to survive the next disaster, but to build operating systems that remain functional under a changing climate.

The Role of Finance

Finance has a central role to play in this dynamic. Green bonds and green loans can fund projects such as energy-efficient buildings, flood defenses, grid resilience, water-saving technologies, and renewable-energy investments. Sustainability-linked loans and bonds can tie financing costs to measurable climate targets, including emissions reduction, energy efficiency, climate-resilient capital expenditure, or adaptation milestones. When used effectively, these instruments can move climate finance beyond symbolic ESG commitments and toward concrete balance-sheet responses.

Conclusion

The broader message is clear. ESG politics may retreat from the boardroom, but climate exposure does not. Companies may talk less about transition risk, but Europe’s heatwave shows why physical climate risk is becoming impossible, and increasingly costly, to ignore. The firms that understand this shift will not treat climate risk as a public-relations problem. They will treat it as a question of valuation, financing, and long-term competitiveness.

Shan Hongyu is an Associate Professor of Finance at CEIBS. His research explores the impact of climate change and other ESG initiatives on financial markets and corporate decision-making. His work has been published in The Review of Financial Studies and Production and Operations Management and has been presented at leading academic conferences, including the American Finance Association Meeting, the Western Finance Association Meeting, SFS Cavalcade, and CICF.