Faculty & Research

Faculty & Research

Should We Be Worried about China's Economic Slowdown?

By Professor of Economics Bala Ramasamy and Cheng Li

Financial markets have become increasingly nervous whenever China reports its quarterly GDP numbers. The nervousness is not surprising since China is the second largest economy, in real terms, or the largest based on PPP. According to the World Bank, in 2014, China’s USD 10 trillion economy makes up 13.25% of world GDP. But to expect an economy of that size to keep growing as fast as it has in the past is just wishful thinking. In fact since the highs of Q1 2010, accumulated quarterly GDP growth has declined every quarter, falling from 12.38% to 6.7% in Q2 2016. Sinologist Dwight Perkins and Harvard economist Robert Barro are among those who share the view that China cannot continue its breakneck growth. Perkins predicts that no matter how “vigorous the reform efforts”, China’s growth will not exceed 7% over the next two decades. Basing his calculations on the last 50 years of China’s growth figures, Barro puts the country’s long-run growth at within 6%. Years of double digit growth may make 6% seem less than impressive. However, one needs to consider the nature of the current Chinese economy and compare it to the past to appreciate the 6% growth seen despite the many headwinds along the way.

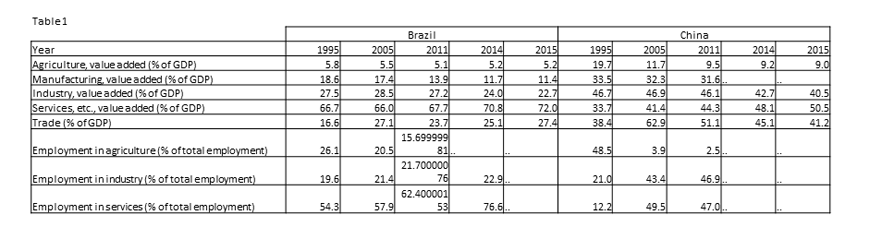

The Chinese economy of twenty years ago was less than 9% of the size it is today, in nominal terms. In real terms, the economy today is more than 6 times larger than it was in 1995. In other words, GDP in 2015 grew an equivalent of the entire Chinese GDP in 1994. Or, viewed from an international perspective, in 1995, China and Brazil were about the same size. By 2015, China was four times larger than Brazil. In 1995, the structure of the Chinese economy was 19.7% agriculture, 46.7% industry (manufacturing and construction) and 33.7% services. Today, the agricultural sector has decreased to the lowest level of 9% while the industrial sector is still holding at above 40%. The services sector has however jumped to more than half of the economy as can be seen in Table 1 below. Meanwhile in Brazil, the services sector has seen large increases while the other two sectors – especially manufacturing – show decline. We can also see the change in the structure of the Chinese economy by looking at the employment figures. Industry and the services sector contribute about the same proportion of jobs in China today. Although trade is still an import engine of the Chinese economy, it contributes markedly less today than a decade ago. The structural shift in the Chinese economy towards services may explain the slowdown in economic growth as services-dominant economies tend to grow slower than manufacturing-dominant economies. A shift towards domestic consumption will naturally result in an emphasis on certain services sectors, like retail and wholesale trade, whose growth will be relatively slower. Thus, a transformation of the economy towards services and domestic consumption will result in slower growth rates – something that should not surprise any observer.

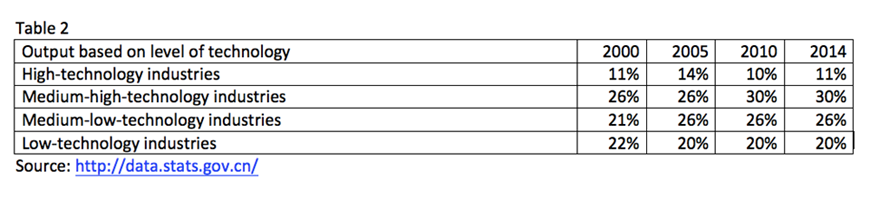

Digging deeper into the manufacturing and services sectors reveals the challenges faced by the Chinese economy (see Table 2). Based on the limited data provided by the National Bureau of Statistics on the market value of various industries, and assigning them to various technological levels as specified by the OECD, we find that there are only small changes in the manufacturing output structure of China. Over the last 10 years, the proportion of output from high-technology industries has actually decreased. The increases are mainly from medium level technology industries. Telecommunication equipment and computers make up a large portion of high technology output. Although there is a more than a 1000% increase in the value of output in this sector (RMB 738.5 billion in 2000 compared to RMB 8527.5 billion in 2014), it has decreased as a proportion of total output. One could also argue that a significant portion of value from this industry could come from mere assembly activities which may not necessarily imply high-technology activity. And while a 1000% increase is impressive, it appears less so when viewed within the context of the more than 3700% increase in the market value of output from the rubber and plastic industries which rely on medium-low-technology. Recent studies on the technological level of China’s exports also conclude that the quality of exports is not very far from other countries at a similar level of development. All this implies that there are still important structural changes required within China’s manufacturing industries. Moving up the technological ladder has to take priority in the years to come.

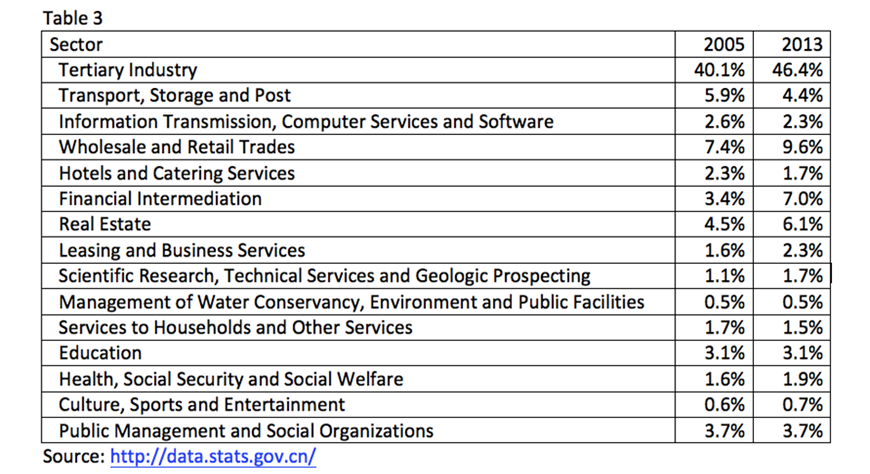

A look at the services sector (Table 3) shows the size of the various subsectors as a proportion of the whole economy, based on current values. The finance and the real estate industries are the ones that have grown most over the time period reported. Wholesale and retail trade is the largest industry and has shown growth, but not large enough particularly if domestic consumption is supposed to be an engine of economic growth. In comparison, the wholesale and retail trade sector comprised nearly 15% of the economy in 2013. In general however, apart from the few industries mentioned, there have been no significant changes in the structure of the services sector over the last decade.

Thus, while we should not be overly worried that the Chinese economy is slowing down as it is just natural for large economies to grow slower as they age, we should be concerned that the structural changes to the economy have not shown significant results, at least not in the macro level indicators. Without structural reforms that raise technology levels and productivity and market reforms that promote entrepreneurial activities resulting in greater transaction of goods and services, the quality of economic growth may suffer the same fate as its quantitative counterpart.

This article was first published by The Economist Intelligence Unit.